Over the past few decades, real estate has been considered a safe haven, a secure and profitable long-term investment. But is Italian property still a safe haven?

However, recent demographic data and market dynamics are calling this assumption into question. According to ISTAT (

see analysis by Tuttitalia.it), the gap between births and deaths continues to widen,

creating a worrying demographic picture for the future of Italian real estate. In many parts of the country, the proposal has even been made to sell houses for one euro in order to repopulate deserted areas — a sign of the deep crisis affecting the sector.

Price trends in the main Italian cities

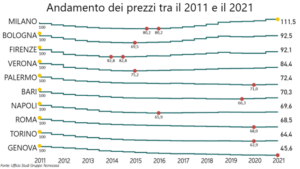

Analysis of property price trends in the main Italian cities over the last ten years shows a mostly negative picture (

see the chart shown alongside, taken from the Tecnocasa Research Department). Taking 2011 as the base year with a value of 100, only Milan recorded an increase in the average value of properties, reaching 111.5 in 2021. Milan, despite a decline until 2016 (80.2), saw a significant recovery, demonstrating a certain resilience of its real estate market.

By contrast, other major cities such as Turin, Rome and Genoa recorded considerable drops. Genoa is the city that suffered the most, with a 54.4% loss in average property value, hitting a historic low of 45.6 in 2021. Turin and Rome saw reductions of 35.6% and 31.5% respectively, with only slight recoveries in the last year of the decade considered.

Cities such as Bologna, Florence and Verona experienced less marked declines. Bologna recorded its low in 2015 (69.5), later recovering to 92.5 in 2021. Florence hit its lowest point between 2014 and 2015 (82.8), then rising again to 92.1. Verona, with a 15.6% loss, saw a steady recovery after 2015, reaching 84.4 in 2021.

The causes of the real estate downturn

The causes of the drop in property prices in major Italian cities are multiple and interconnected:

- Polarisation between large cities and smaller towns: Metropolises such as Milan attract investment, leaving smaller towns with a weak real estate market.

- Difficulties in the labour market: The economic crisis and the casualisation of work reduce families' ability to buy property.

- Exodus of skilled workers abroad: The brain drain abroad reduces housing demand, especially in less developed areas.

- COVID-19 Pandemic: The pandemic has worsened economic uncertainty and shifted housing preferences towards less densely populated areas.

- Demographic changes: The declining birth rate and the ageing population are reducing demand for new housing.

- Bureaucratic inefficiencies and inadequate housing policies: Long administrative procedures and a lack of incentives hold back the development of the real estate market.

Alternatives to real estate investment

In light of this data, the question "is Italian real estate still a safe haven?" finds a decidedly negative answer for most Italian cities, with the exception of the Milan phenomenon. Investors who have until now relied on real estate now need to consider more promising alternatives, which, moreover, are no longer riskier (based on the statistical data).

One option is investing in securities, which offers the chance to diversify the portfolio and achieve attractive returns, especially in a context of global economic recovery. Another valid alternative is represented by mergers and acquisitions (M&A) with investments in small and medium-sized enterprises (SMEs), which can offer significant growth and return opportunities, especially in innovative and expanding sectors.

Conclusion

The Italian real estate market, with the exception of Milan, presents numerous issues that cast doubt on its solidity as a safe haven. Investors must therefore look beyond real estate, carefully assessing other forms of investment capable of offering stability and growth. Only through prudent diversification and a careful evaluation of the alternatives will it be possible to protect and grow one's wealth in an increasingly uncertain economic and demographic environment.